Climate and regulation: supply chain traceability at the heart of reporting

Agricultural, forestry, and agri-food companies operate in an increasingly complex regulatory and methodological environment.

In recent years, they have had to adapt to a growing number of requirements: the EU Deforestation Regulation (EUDR), climate reporting, SBTi FLAG targets, and product carbon footprint calculations. These initiatives are often led by different teams, pursue distinct objectives, and rely on their own specific frameworks.

At first glance, they can therefore seem largely independent of one another.

Yet an underlying trend is emerging. Whether the goal is to demonstrate that a raw material is compliant, assess a product’s carbon footprint, or steer a decarbonization trajectory, companies increasingly need the same information: where their raw materials come from, which territories they depend on, and how those territories change over time.

The publication of the GHG Protocol’s new Land Sector and Removals Standard (LSRS) illustrates this shift. Far more than a simple methodological update, this standard reflects the growing importance of land and traceability data in managing climate-related issues.

Two complementary views of carbon

To understand what the LSRS changes, it helps to distinguish between two main ways of approaching carbon.

The product view: Life Cycle Assessment (LCA)

Life Cycle Assessment (LCA) answers a simple question:

What is the carbon footprint of my product?

This approach attributes environmental impacts to a functional unit — a kilogram of cocoa, a metric ton of palm oil, or a chocolate bar, for example. It is used for environmental labeling, eco-design, product environmental declarations, and customer requests.

The goal is to understand the impacts associated with a product across its entire life cycle.

The company/organization view: GHG Protocol, LSRS, and FLAG

Corporate carbon accounting answers different questions:

- What are my company’s emissions?

- What are the land-related impacts of my supply chains?

- How do I reach my climate targets?

This is the space in which the GHG Protocol, the LSRS, and SBTi FLAG targets operate.

The climate reporting ecosystem has been built up in stages. The GHG Protocol, published in the early 2000s by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), has become the global reference for corporate carbon accounting. It defines the principles for calculating Scope 1, 2, and 3 emissions. For a long time, however, this framework remained less detailed when it came to emissions from land, agriculture, and forestry. To address this gap, the GHG Protocol developed the Land Sector and Removals Standard (LSRS), published in early 2026. This new standard specifies how to account for emissions, carbon removals, and stock changes associated with land, forests, and agricultural activities. In parallel, the Science Based Targets initiative (SBTi) was created in 2015, also under the WRI’s umbrella, alongside the NGO WWF, to help companies set climate targets aligned with the Paris Agreement. In 2022, the SBTi published the FLAG guidance (Forest, Land and Agriculture) to more explicitly integrate land-related, deforestation, and agricultural emissions into companies’ climate trajectories. |

The LSRS complements the GHG Protocol for land-related carbon emissions and removals: land-use change, management practices, soil carbon, and carbon removals. FLAG, meanwhile, provides a framework for defining and steering the reduction trajectories associated with these emissions.

These approaches pursue different objectives but increasingly rely on the same underlying data: plot locations, land-use history, land-use change, and supply chain traceability.

This is precisely why a single company can now have several different carbon figures without those figures necessarily being contradictory.

Companies are often surprised to find that their product carbon footprint, their corporate carbon footprint, and their climate targets don’t tell exactly the same story. These three approaches answer different questions, much as financial accounting relies on several complementary tools to manage a business.

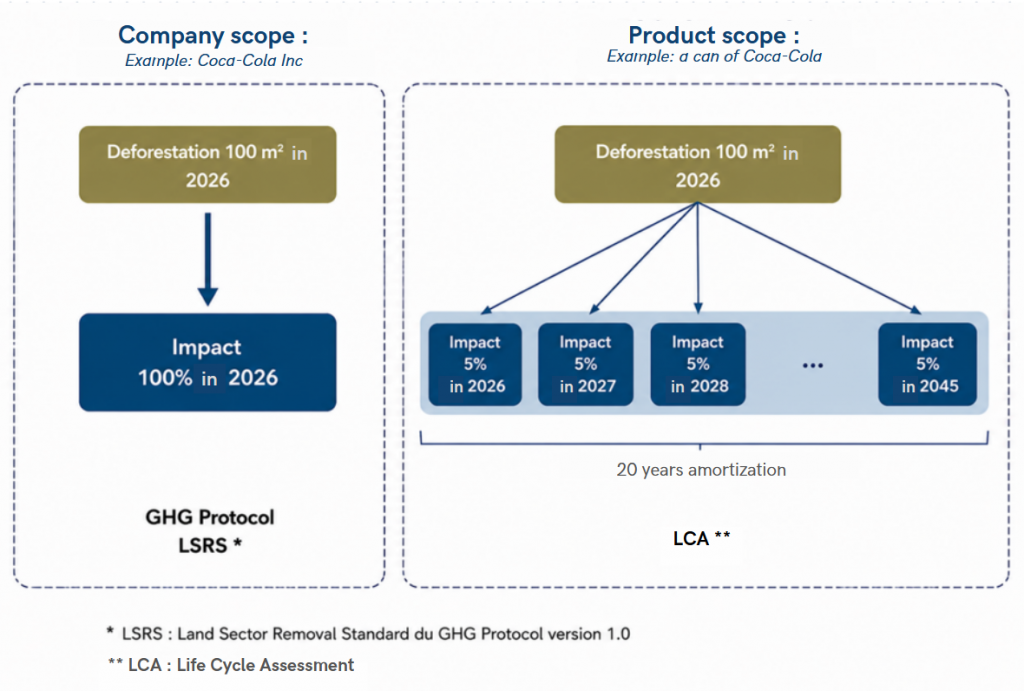

LCA seeks to attribute environmental impacts to a product: it answers the question “What is the carbon footprint of this product?” The GHG Protocol and the LSRS seek to represent the emissions and carbon removals associated with a company’s activity: they answer the question “What are our emissions?” SBTi FLAG does not measure emissions. It sets a reduction trajectory: “Where should we be by 2030 or 2050?” Numbers produced by these approaches are therefore not meant to be identical. They generally draw on the same data (such as plot location or land-use change) but to serve different purposes. Take the example of a land conversion that occurred in 2026. In a corporate carbon inventory, the impact would generally be accounted for when it happens. In an LCA, that same impact might instead be spread over several years and allocated to the products that benefit from that land.

Figure 1: Diagram of the impact scopes measured by the GHG Protocol and LCA

Different results therefore don’t necessarily mean an inconsistency. They simply reflect different ways of analyzing the same reality. |

What does the LSRS actually change?

For a long time, corporate carbon accounting has been relatively well equipped to measure emissions from energy use, industrial processes, or transport. Land-dependent activities — agriculture, forestry, land-use change, or soil carbon storage — remained, by contrast, harder to capture consistently.

It is precisely to address this gap that the GHG Protocol developed the Land Sector and Removals Standard (LSRS).

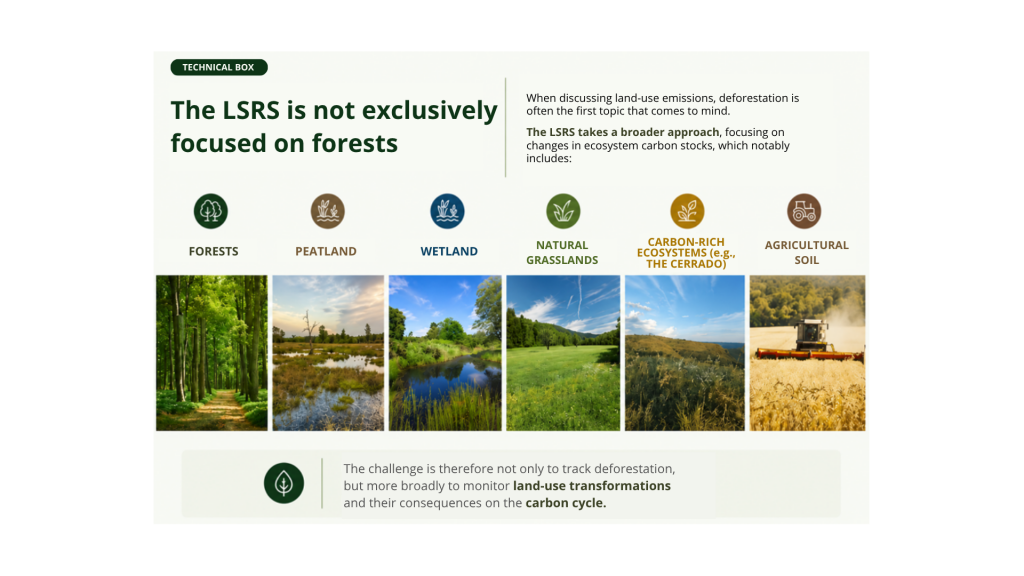

Figure 2: LSRS technical box

Figure 2: LSRS technical box

The LSRS provides a harmonized framework for accounting for the main sources of land-related carbon emissions and removals. It covers in particular:

- land-use change (LUC);

- land management practices;

- carbon removals;

- carbon stocks held in soils and biomass.

Beyond these technical concepts, its main contribution lies elsewhere: it offers a common language for describing how companies interact with the land they depend on.

The LSRS makes it possible to better connect emissions linked to agricultural or forestry supply chains with companies’ climate strategies. It also helps strengthen consistency between carbon accounting, FLAG targets, and the reduction or sequestration initiatives implemented on the ground.

In other words, the LSRS doesn’t just introduce new calculation rules. It marks a deeper shift: accounting for land and how it is managed is gradually becoming a central part of corporate climate accounting.

A convergence around land data

EUDR, LSRS, FLAG targets, and many LCAs pursue different purposes. The EUDR aims for regulatory compliance; the others, carbon accounting or the steering of climate trajectories.

Yet they increasingly rest on the same foundation of information.

To demonstrate that a raw material is not linked to deforestation, to calculate emissions from a land-use change, or to understand a product’s climate impacts, companies often need to draw on the same data:

- geolocation of plots;

- land-use history;

- land-use change;

- traceability of raw materials throughout the supply chain.

Yet, calculation methods remain different. So do results.

But the data needed to produce them is increasingly converging.

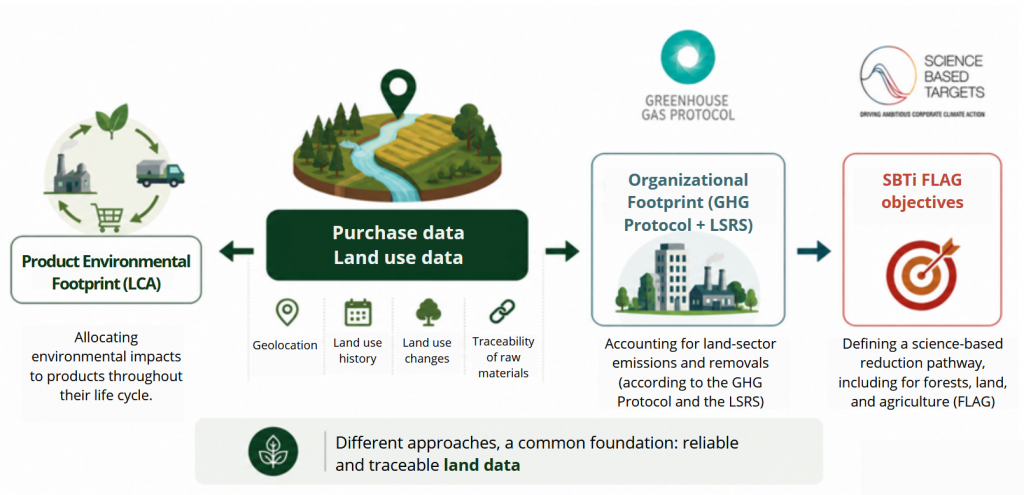

Figure 3: Diagram of the different land data approaches used by LCA, LSRS, and SBTi FLAG

This shift is particularly visible in the agricultural and forestry sectors, where understanding emissions increasingly depends on the ability to connect products to the territories they come from.

In other words, the location and history of land are becoming progressively as important as the volumes purchased or the emission factors used.

This convergence of regulatory and climate requirements is accompanied by a rise in geospatial data. Access to geolocated information on the territories where raw materials originate now makes it possible to enrich traceability efforts, improve understanding of land-use change, and strengthen the robustness of climate analyses. As this data becomes more precise and more widely available, it is expected to play a growing role in compliance, reporting, and environmental risk management processes. |

Beyond compliance

For many companies, the investments made to comply with EUDR were initially seen as just another regulatory burden. Collecting GPS coordinates, mapping supply chains, or analyzing land-use change were seen, above all, as a necessary cost to demonstrate that supply chains were compliant.

The LSRS invites a different perspective on these investments. The data gathered to comply with the EUDR is also the data that helps companies better understand land-related emissions, strengthen the quality of their carbon inventories, and feed the reduction strategies tied to FLAG targets.

In particular, it helps to:

- better identify emissions associated with land-use change;

- understand the impact of land management practices;

- track changes in carbon stocks;

- strengthen the credibility of climate reporting;

- more directly connect carbon issues to supply chains.

For companies dependent on agriculture and forestry, traceability is therefore no longer just a compliance tool. It is gradually becoming a lever for climate strategy.

Organizations that have already begun mapping their supply chains to comply with EUDR may already hold part of the data they will need to meet the climate requirements of the coming decade.

References

GHG Protocol

LSRS: Land Sector and Removals Standard of the GHG Protocol, version 1.0

https://ghgprotocol.org/land-sector-and-removals-standard

SBTi

https://files.sciencebasedtargets.org/production/files/Net-Zero-Standard.pdf?dm=1776156995

SBTi FLAG

https://sciencebasedtargets.org/sectors/forest-land-and-agriculture

EUDR

![]() Member of the European PEF (Product Environmental Footprint) Technical Advisory Board.

Member of the European PEF (Product Environmental Footprint) Technical Advisory Board.

![]() Member of the French ADEME environmental labelling working group.

Member of the French ADEME environmental labelling working group.